Is Lagos the hottest hotel development market in Africa? Look at the fundamentals: a city of some 15 million inhabitants, projected to be one of the world’s 10 “mega cities” by 2025; the commercial centre of the continent’s second-largest economy; the main aviation and shipping hub for West Africa, with a compound increase of 10 per cent in international arrivals in the last 10 years; and with occupancies in the city’s hotels running at 85+ per cent year round.

Demand for Lagos’ hotels is generated by three main sectors – telecommunications, banking, and, of course, oil and gas. The latter is the driver of Nigeria’s economy, with oil output of 2.5 million barrels per day (mbpd) due to double by 2010, and major expansion in gas production.

Yet no major new hotel has opened in Lagos since the Sheraton in 1985. So demand outstrips supply, leading to high rates for rooms, and high profits for owners. The leading hotels are charging US$300 to US$400 per night for a standard room, and despite some high operating costs, particularly energy and maintenance, that translates into high profits. Large hotels in Lagos can produce operating profits of 55 per cent and more, compared with European hotels averaging in the order of 35 to 40 per cent.

There are several new hotels under construction, but many are delayed from their originally-projected opening date. Why? Most often due to a lack of funding. Whilst in most markets hotel developers secure the total funding before starting work, it seems to be the norm that only part of the funding is secured, and developers underestimate the time it takes to raise the balance, leading to (expensive) delays in completion, most often measured in years. Other expensive mistakes include not bringing the hotel operator on board from the outset, and very often the operator requires changes to the existing structure in order to meet brand standards.

What’s the solution? Clearly, it makes better sense to raise 100 per cent of the finance prior to starting work on site, or at least before starting the superstructure. And it is never too early to bring the operator on board, to save expensive alterations later on, and even to save money through better design and procurement.

Lagos is, indeed, the hottest market in sub-Saharan Africa, and there are multiple opportunities for new investors to enter the market, from boutique hotels, catering to the discerning executive traveller, to large internationally-branded operations for the corporate and conferencing market. Problems in the Niger Delta are forcing many companies to relocate their operations to Lagos, resulting in higher demand for hotel accommodation at all levels. Proper planning of a project, avoiding the mistakes of others, could well mean that your new hotel will open before some of those currently under construction!

Each year we collect information from the major international and regional (African) hotels chain, to find out what they are doing in terms of signing new deals for the branding and management of new hotels in Africa. At the beginning of 2013, the chains which contributed to our survey reported a total of 207 hotels in their development pipelines in Africa, with almost 40,000 rooms. This includes only those binding deals which have been signed between a hotel chain and an owner, and is up almost one third on two years ago. In a dynamic market, with an increasing number of players, new management and franchise opportunities appear every day, but these are the ones with full approval and which are more likely than not to proceed.

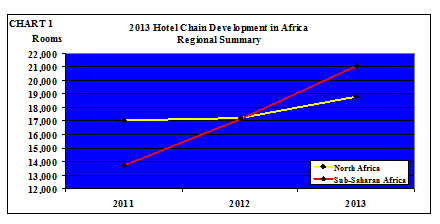

Table 1 shows the “Tale of Two Africas” – the distribution of the deals between North Africa and the rest of the continent.

TABLE 1

2013 Chain Hotel Development in Africa

Regional Summary

2013

2012*

2011*

Hotels

Rooms

Hotels

Rooms

Hotels

Rooms

North Africa

77

18,782

77

17,217

75

17,038

Sub-Saharan Africa

130

21,052

100

17,109

76

13,700

TOTAL

207

39,834

177

34,326

151

30,738

* In all the tables we have rebased previous years’ data to include 2013 contributors only

The pipeline in North Africa has experienced relatively little growth, for two reasons – several hotels in previous years’ pipeline data opened in 2012 (Accor alone opened 8 hotels with 1,153 rooms in Algeria, Morocco and Tunisia), and the political turmoil in the region has had a negative effect on new investment and, therefore, new deals.

In North Africa, the development pipeline grew by 9 per cent in 2013. In sub-Saharan Africa, however, the increase was a massive 23 per cent. This compares to 4 per cent growth in Europe and 8.6 per cent growth in Asia Pacific, according to pipeline data produced by STR Global (although the growth in Africa is from a much lower base).

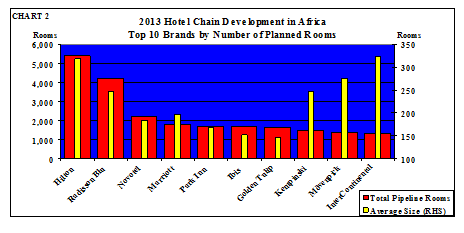

The top ten brands by number of hotels and rooms in their pipelines are shown in Table 2 and Chart 2.

TABLE 2

2013 Chain Hotel Development in Africa

Top 10 Brands by Number of Planned Hotels and Rooms

Rank by Hotels

Rank by Rooms

Change on 2012

Average Size

1=

Hilton

17

1

Hilton

5,400

68.4%

318

1=

Radisson Blu

17

2

Radisson Blu

4,191

11.5%

247

3

Novotel

12

3

Novotel

2,192

7.6%

183

4=

Ibis

11

4

Marriott

1,767

41.4%

196

4=

Golden Tulip

11

5

Park Inn

1,676

11.9%

168

6

Park Inn

10

6

Ibis

1,675

8.7%

152

7=

Marriott

9

7

Golden Tulip

1,608

88.7%

146

7=

Kempinski

6

8

Kempinski

1,481

8.0%

247

7=

easyHotel

6

9

Mövenpick

1,369

-37.3%

274

10

Mantis

6

10

InterContinental

1,296

-35.5%

324

Table 2 and Chart 2 analyse the pipeline by brand. The number one slot is occupied by the Hilton core brand on its own – the performance of Hilton Worldwide, and its pipeline in three brands (Hilton, Doubletree by Hilton and Hilton Garden Inn), is analysed in Table 4.

Two brands are first equal in terms of the number of hotels in the pipeline, but whilst this is an indication of how large the system footprint is set to grow, the number of rooms is a better

indication of future earnings, and Hilton outstrips Radisson Blu by almost 30 per cent on that measure, because of the larger average size of their planned hotels.

The above analysis is of brands – many of the hotel companies are multi-brand players, so it is relevant to look at it per group as well. It is noticeable that the global chains are now entering the African market with more of their brands – Hyatt have signed their first Hyatt Place deal, Hilton are moving ahead with Hilton Garden Inn, and Louvre are bring Campanile and Première Classe to Africa. This gives owners greater choice, whilst still receiving support from a major group.

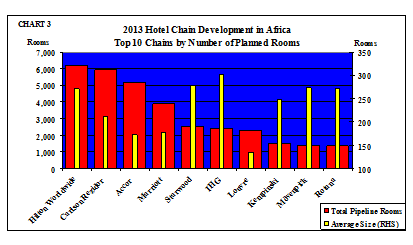

Table 3 and Chart 3 show the pipelines by hotel chain.

TABLE 3

2013 Chain Hotel Development in Africa

Top 10 Chains by Number of Planned Hotels and Rooms

Rank by Hotels

Rank by Rooms

Change on 2012

Average Size

1

Accor

30

1

Hilton Worldwide

6,230

84%

271

2

Carlson Rezidor

28

2

Carlson Rezidor

5,947

11%

212

3

Hilton Worldwide

23

3

Accor

5,165

-14%

172

4

Marriott

22

4

Marriott

3,900

55%

177

5

Louvre

17

5

Starwood

2,514

17%

279

6

Starwood

9

6

IHG

2,413

-16%

302

7=

Best Western

8

7

Louvre

2,290

146%

135

7=

IHG

8

8

Kempinski

1,481

8%

247

7=

Lonrho

8

9

Mövenpick

1,369

-37%

274

10

Kempinski

6

10

Rotana

1,355

8%

271

All the majors are there, dominated by Hilton Worldwide and Carlson Rezidor, both of which have invested heavily in establishing development offices in Africa. Best Western enters the ranking with eight signed membership agreements and almost 800 rooms, of which all but one property is under construction. Six new African Best Western hotels are due to open in 2013, taking the total to 14 hotels with over 1,500 rooms.

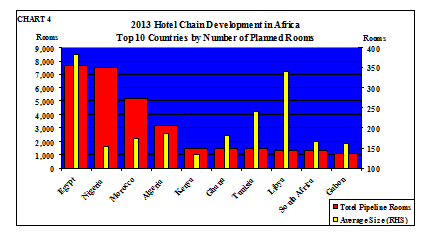

Where is all this activity taking place? Of the total pipeline, 47 per cent is in the five countries of North Africa, and 53 per cent in the 49 countries of sub-Saharan Africa. Table 4 shows the top ten countries.

All of the five North African countries feature in the top ten destinations for branded hotel developments, the majority of activity are located in Egypt and Morocco, where the tourism industries are most well-established.

TABLE 4

2013 Chain Hotel Development in Africa

Top 10 Countries by Number of Rooms

Hotels

Rooms

Average Size

1

Egypt

20

7,644

382

2

Nigeria

49

7,470

152

3

Morocco

30

5,178

173

4

Algeria

17

3,160

186

5

Kenya

11

1,469

134

6

Ghana

8

1,441

180

7

Tunisia

6

1,441

240

8

Libya

4

1,359

340

9

South Africa

8

1,320

165

10

Gabon

7

1,128

161

Nigeria, Africa’s largest country by population, the power house of West Africa – and tipped to overtake South Africa this decade as the largest economy on the continent – has almost 7,500 rooms under contract, up 10 per cent on last year’s figure, with at least two more deals signed since the beginning of 2013 (not included in the above data), and thousands more in the “nearly” category.

Note that hotels being planned or developed in North Africa are typically larger than those in sub-Saharan Africa, particularly in Egypt. Nigeria may have the largest pipeline in sub-Saharan Africa, but the average size of hotel there is relatively small. Conversely, however,

one of the largest hotels in West Africa, the InterContinental Lagos with 358 rooms, is due to open in 2013.

New to the Top Ten in 2013 are Kenya and Gabon. Nairobi is the focus of attention in Kenya, with seven companies entering the market there – Best Western, Country Lodge, Accor (Novotel and Ibis), Carlson Rezidor (Radisson Blu and Park Inn), Dusit, easyHotel and Kempinski. With almost 1,500 rooms between them, of which almost 700 are due to open in 2013, is an oversupply situation looming?

On average, the global hotel brands have less than 2 per cent of their total rooms in sub-Saharan Africa, and with rapid expansion of their existing and upcoming hotels in China, India and other developing and developed countries, this percentage could drop further. But the rewards in Africa are high, and with economic growth rates in many countries of 7 per cent and above, it is regarded by many as the most profitable place to do business – just slower than “normal”.

Many projects in sub-Saharan Africa are delayed from their original opening date, for a variety of reasons. But we see that improving, as more sophisticated investors, including specialist funds, enter the market, capable of running a successful development project. We have identified five hotel funds currently active in Africa, with others being established, seeking acquisition and new-build opportunities. In addition, several international construction companies, from Europe, the Middle East and elsewhere, are eying the market, bringing construction finance with them.

Since we first started the hotel pipeline survey in 2009, we have seen the number of rooms increase from 30,000 rooms to 40,000 rooms, and in the intervening four years, the hotel chains have opened an estimated 20,000 rooms in Africa.

Africa is firmly on the agenda!

*****************

Notes on the sample:

We sent questionnaires to 42 international and regional hotel chains, of which 29 submitted data. In addition, three international chains provided a zero-deal return, and two South-Africa based chains declined to participate this year (although they had participated in the past). We polled only those international chains with an interest in being in Africa, or Africa-based chains with operations and/or deals outside their home country.

This report summarises the results of our analysis. Detailed information on all the deals signed by the chains are provided only to the contributors.

Welcome to the 2017 edition of our annual Hotel Chain Development Pipelines in Africa. This ninth edition of our annual survey has 36 international and regional contributors, reporting pipeline activity of almost 73,000 rooms in 417 hotels, a 13 per cent increase on the 2016 pipeline.

The market and financial feasibility study is an essential first step in the process, after securing the site, and we specialist in the preparation of such studies.

There are five main reasons for carrying out a feasibility study of a hotel project: for the benefit of the promoter, to ensure full understanding of the risks and rewards of the project; to determine the most appropriate facility provision for a given site and market; to brief the architect as to what the market requires in terms of facilities; to attract the attention of an operator and to form the basis for contract registration; and to support submissions to debt and equity providers.

In general terms, the output of a feasibility study is information, conclusions and recommendations on:

• the current and projected future economic, political and social environment in which the proposed hotel will operate;

• the location for the proposed development, and the strengths and weaknesses of the site;

• the current and projected future market environment in the project location, with a detailed supply and demand analysis;

• product concept and market positioning, the number and type of guest rooms and other facilities;

• operating factors of relevance, including aspects of management and marketing of the property;

• projections of revenue, cost, profit and annual cash flow, and a calculation of the resultant return on investment.

On completion of the market analysis and the feasibility study, we will spend time with you to discuss our report, to ensure that you fully understand our conclusions and the assumptions on which they are based.

If necessary, we will undertake additional financial modelling according to your requirements. This would include different financing scenarios, as described below.

Our study will be prepared assuming development of an agreed mix of facilities and services. Following discussion of our conclusions, we can carry out further financial modelling, and look at different physical scenarios, including phasing of the development, as considered appropriate. We will work closely with the project architect, to get the design and the detailed specification right. This will be an iterative process, taking account of the research as well as your own requirements, and should ideally include the selected hotel operator.

The nature of hotel project cash flows is such that the financial structure needs careful analysis to avoid, for example, over-burdening the business with debt, and to ensure correlation with the owners’ and investors’ return requirements. Part of the additional modelling would include working with you to derive a financial structure for the project which is both supportable and also achievable.

For selected projects, we are able to introduce sources of debt, and to negotiate terms on your behalf.

We can provide valuation advice throughout the development process and after completion. Our property department is staffed by RICS (UK) qualified Registered Valuers who provide formal valuation advice that is compliant with the requirements of the vast majority of lending institutions. Formal valuations are often required by lenders as part of their loan monitoring process, to ensure that loan-to-value covenants are adhered to.

There are numbers of possible ways to provide management to a hotel, ranging from appointing a management company, to the owner running it personally.

For this development, we understand that you would want to delegate the operation of the hotel to a professional management company.

In the first instance we will undertake desk-based research in order to prepare a list of operators that we think would be appropriate for this project, and who would be interested in the opportunity. We will agree that list with you, and contact each operator to gauge their interest in principle, and the brands that they could offer.

For those with whom it is considered appropriate to pursue discussions, we will prepare a brief detailing each brand’s system size, main characteristics of their brand, and their strengths and any weaknesses relative to this project.

We will also prepare a project dossier to send to them, which will include the feasibility study, or extracts therefrom.

We will write to each of the short-listed companies, providing them with the project dossier and inviting them to submit their tender for the management of the proposed hotel by a stated deadline. It is our usual practice to prescribe the form of their response, so that comparison is easier.

We will analyse the responses, present that analysis to you and discuss it with you, and assist you to select an operator with whom negotiations can commence. We will lead those negotiations, in order to obtain the best commercial deal, and fair terms of contract. You will in addition need to engage the services of legal counsel to ensure that the contract is in accordance with local law.

The output of this work is a management agreement which you can sign with confidence.

We can provide full development management services, handling negotiations with contractors, consultants, suppliers and others, managing the project budget, reporting on programme and quality, providing a coordination point for all involved in the project, and overseeing the design and the finishes.

We have very strong relationships with global manufacturers and suppliers. Based on these, we can eliminate the cost of the middle-man, managing the entire process of FF&E and OSE procurement, ensuring that brand standards are met. We also provide an installation service, receiving and installing all FF&E, testing equipment, training staff in equipment operations, and preparing asset registers.

Once the hotel is open, we can provide asset management services, essentially “managing the manager”, ensuring contract compliance, and that the Owner’s requirements are met, in terms of financial returns. This is a pro-active role, both monitoring and assisting the management team on ground to meet objectives.

Trevor Ward on CNBC Africa’s Open Exchange.

Trevor Ward talks about how Africa’s Hotel development has been stalled on CNBC Africa’s Open Exchange.

Trevor Ward is a specialist consultant in the hospitality and leisure industries and is the Principal of the W Hospitality Group.

He started his consultancy career in 1983, having previously completed a university degree in hotel management at the University of Surrey, and worked in management positions with De Vere Hotels and Ladbroke Hotels in the UK. From the late 1980s he has specialized in the provision of advisory services to clients in developing countries, and since 2003 has been based in Nigeria, advising clients there and throughout Africa.

His international experience includes advising clients on hotel and tourism development in more than 90 countries in Europe, North and South America, the Caribbean, Africa, and Asia. With a special focus on sub-Saharan Africa, he is working with many of the international hotel groups who are seeking a presence there, from the oil-rich countries of the west to the tourism hotspots of the south and east. He is regarded as one of the foremost experts on the hotel industry in sub-Saharan Africa and is engaged primarily in development consultancy ranging from investment appraisals to operator selection, owner’s representation, and asset management.

In addition to his advisory work, Trevor is an active member of the Institute of Hospitality, for which he is their Ambassador for Africa, and of the International Society of Hospitality Consultants. He is also closely involved with industry organisations such as the Hotel Owners and Managers Association of Lagos, the West Africa Tourism Organisation and the African Travel Commission.

Trevor is a regular speaker at industry conferences and writes in various professional and Africa-focused journals, including African Business Traveller and Africa Investor.

Ilobekeme Odiase is an experienced management consultant with over 10 years’ industry experience including a Masters’ degree in Management from the Robert Gordon University, Aberdeen.

Ilo joined W Hospitality Group in 2013 where she works on the preparation of market and financial feasibility studies for proposed hotels, convention centres and mixed-use developments in Abuja, Accra, Banjul, Kigali, Lagos and other sub-Saharan markets.

Her professional experience covers real estate and workplace services management, from working with SAP and Hewlett Packard in various capacities. Ilo is a member of the Chartered Management Institute, UK and loves to read in her spare time.

Affiliated to

1 Resort Court Plot 15 Block XV Chief Yesufu Abiodun Way Oniru Estate Lagos,Nigeria

.

.