Having experienced several years of stagnation, Kenya’s tourism industry was on a veritable bull-run. One million visitors in 2002 increased to an estimated two million in 2007, accompanied by an increase in the length of stay from 8.5 nights to 12.1 nights (2006). And that in turn meant a tripling of earnings, vitally important to the country’s goal of eliminating poverty.

In the late 1980s and early 2000s, Kenya had been bevelled by external shocks – the US Embassy bombing in 1998, the effects of the September 2001 attacks in the USA, and the attacks in Mombasa in late 2002. The country, largely the private sector, did what it could to minimise the effect on the tourism industry, but it was not as effective as it could have been.

And then the boom between 2004 and 2007, with increased government contribution to promoting the country’s tourism product. But in late 2007, Kenya’s international image, and by direct association its tourism industry, was severely damaged, this time by an internal shock, the civil unrest that followed the December elections. Tourist numbers and receipts were down by one third in the first half of 2008, resorts were closing down, staff laid off, and it looked like Kenya had “had it”.

But this time the government led the attack, perhaps learning from the experiences of Egypt, so often affected by both internal and external shocks, and each time bouncing back with a vengeance. Tourism to Egypt was devastated by various terrorist attacks in the 1990s, culminating in the Luxor massacre in 1997 when 58 foreign tourists were killed. But in the relative peace thereafter, the country doubled the number of international visitors, by restoring confidence in the tourism product, with the general public and the travel trade.

Kenya has done the same, with massive efforts by the government to assure the world that the country is safe to visit. The last travel advisory, warning US tourists not to travel to Kenya, was lifted in mid-2008, and the industry is expecting recovery to commence in earnest with the winter season this year. The government has invested in promoting the country – a reported spend of well over US$10 million dollars from government funds, and a further US$10 million from the EU, just on marketing.

And at the same time, the local and global hospitality investment industry is expressing just that confidence that the government is seeking to engender, by announcing new deals in the country – Kingdom are investing in the refurbishment of their five hotels in the country, Radisson SAS are to manage a new luxury hotel under

construction in Nairobi, owned by Elgon Investments, and Kempinski and Accor are known to be eying up the market.

Tourists have, thankfully, short memories. They are receptive to marketing messages extolling the virtues of a destination, even when that destination has been portrayed negatively by the same media as are now pushing its benefits. Kenya has just spent over US$2 million on an advertising campaign on CNN – always the first into trouble spots like……Kenya.

How can investors rake the risk of developing new hotels and other facilities in Kenya, when the troubles at the turn of the year are just a few months old? It is because of that short-term memory, that enables a destination such as Kenya, which offers experiences of great depth and impact, and cannot easily be replicated. And it is because, throughout all the problems of the early part of the year, the Kenyan authorities were able to maintain economic stability, so important to investors – the probable recession that so many forecasters foretold has not come about, and forecasts of economic growth for 2008 range between 4 per cent and 7 per cent – not bad for a country with a 1 per cent decline in the first quarter of the year.

And investors are encouraged also by the realisation that Kenya has a large and growing domestic tourism industry, which is not susceptible to the threats which can so easily damage international tourism. Kenyans are the largest users of hotels in the country by far, and also one of the fastest growing markets, increasing from 800,000 bednights in 2000 to almost 1.4 million in 2006. Whilst international tourists bring much-needed foreign currency, a domestic tourist creates the same number of jobs from his or her overnight stay, and the demand is less seasonal. This strong foundation of domestic tourism can significantly reduce investor’s risk.

Everyone lost money in the first half of the year in Kenya. But tourism is a long-term investment, and it is a fact that challenging times are often good for the industry, forcing a reappraisal of product and marketing strategies, and producing a leaner, fitter set of players, ready for the next race.

Kenya, definitely a tourism investment destination of the future.

Trevor Ward

W Hospitality Group, Lagos

Who would have thought it? The government of Kenya is shaken to its core, the Finance Minister has had to step aside after a vote of no-confidence, a foreign country’s (Libya’s) sovereign fund, is involved in the scandal, and a commission of enquiry has been established, all because of the sale of a hotel. Our industry is not usually the subject of political debate and scandal, but then these are obviously special circumstances.

The hotel in question is the Grand Regency in Nairobi, a 226-room property in the centre of the capital. And the hoo-ha is over two things – first that the way in which the hotel was sold was improper, and second that the amount for which it was sold – KSh2.9 billion – was way below its “real” value. Steering well clear of the first point, I will focus on the second, that of valuation, and try to shed some light on this suddenly controversial subject

Critics of the deal, who seem to have become instant experts on the subject of hotel valuation, have bandied about figures twice or three times that figure as the real “value”, and are therefore claiming that the government has been short-changed. Investors in Africa’s hotel industry need to be mindful of the fact that government-owned hotels – and there are many of them around the continent – are highly visible to the public and to the local politicians, and that their sale can be highly emotive, more so perhaps than assets in other industries. Any price offered for hotels needs to reflect the true value, and to be supportable by the facts.

Let’s look first at the difference between “value” and “worth”. I can value anything I own at whatever price I like, and can be content with my personal delusions, but at the end of the day, the realisable value is only as much as the amount it is worth to someone else, that is, what they are prepared to pay for it. Fairly elementary, no? In the High Street, the shopkeeper prices his goods at a level that people will buy them for – any higher, then they will not sell. Still pretty elementary, I believe.

The difficult part comes when you want to work out what that “sticker price” should be. Well, international hotel valuers – and I count myself as one – mostly use the income capitalisation approach to valuation. What we say is – the value of a hotel is

what a rational buyer is prepared to pay for it, who is buying the hotel to make a return on his investment. That return will be generated by the profit from the hotel’s operations. So what is the earnings capacity of that hotel?

Expert hotel valuers look at the condition of that hotel, the way it is managed, its market positioning and competitive situation, the additional investment required to

sustain or enhance earnings, we make projections of future profitability, and then apply some truly complicated algebra to all that figuring (thank goodness for computers!), to come up with the amount of money that a willing buyer would pay a willing seller in the expectation of making x% return.

I’m not privy to the earnings figures of the Grand Regency Hotel in Nairobi, any more than are the majority of the “instant experts”. But what I can do is look at the figure for what it was reportedly sold, compare it with other hotel transactions, and generally judge it for reasonableness in light of what I know about the Nairobi market. Ksh2.9 billion is about US$46 million, which means about US$200,000 per room – and we look at it per room because it is the sale of rooms to overnight guests that is the primary generator of profits in the hotel. I understand from press reports that the hotel is a bit tired, and needs money spent on it if it is to compete properly with the likes of the (refurbished) InterContinental, the upcoming Radisson SAS and other future competitors. So a new owner may end up spending something like US$250,000 per room by the time they’ve finished.

One thing to note about the African hotel market is that the number of transactions against which to compare this figure – US$250,000 per room – is very small. Hundreds of hotels worth billions of dollars are sold each year in Europe and the USA – the annual number of hotel sales in the whole of sub-Saharan Africa, excluding South Africa, is probably less than twenty. So there isn’t much to compare the sale of the Grand Regency with. But there is one, the sale of the former Lonrho Hotels portfolio in Kenya to Kingdom Holdings. A total of 440 rooms and suites was sold in mid-2005 for an average of less than US$80,000 per room. Even with inflation, that’s less than US$100,000 per room today. This price reflected the earnings potential of the five hotels, the condition of the physical asset and the capital a new owner would be required to inject to achieve that potential. The exact same factors which any rational investor would have taken into account when sizing up the Grand Regency Hotel.

So on the face of it, KSh 2.9 billion looks about right to me. And the implied amount per room – US$427,000! – from the suggested “proper” value of KSh7 billion certainly does not! But we need more information to accurately judge what the hotel is worth, and the moral of this story is that potential investors cannot determine the true value to them without full disclosure. Buyers and sellers beware!

Trevor Ward

W Hospitality Group, Lagos

This is just not fair. You hear me? It’s not proper!

Travelers like me are proud of the hardships we endure, trekking around this continent, it’s what keeps us going, and we enjoy telling and retelling our “war stories”, of airports and hotels in dodgy places.

And then this happens.

They opened a new airport terminal in Luanda. No more scrums, no more daft forms to fill in, polite immigration officials, passport scanners, stamp, stamp and whoosh – I was through in two shakes of a lamb’s tale. Once again I had forgotten my vaccination certificate, and even then it took just 5 minutes and US$50 to get a new one (did I get an injection? Of course not!), from a very smiley doctor, who agreed that the health official who had very officiously marched me in to him, with lots of finger wagging, was a bit loco.

Extraordinary, in and through in less than 15 minutes. Shocked! Let’s just hope that there will be something to complain about at the new Luanda airport the Chinese are building at Viana (or not building, as the case may be – I hear the project is as good as abandoned).

But the Hotel Presidente still manages to triumph in the anti-customer care department, with the receptionist his usual unwelcoming, laid back self (he’ll check you in when HE feels like it, which is not necessarily the same thing as when YOU ask for it!), and the porter actually asking for a tip. Not a single staff member ever smiles, the barman is rude, the internet doesn’t work, the laundry isn’t operating. Just try to stay away from them, they might do the decent thing one day and go away. On check-out, not a single word of apology for overcharging me on every single item on my bill.

Happily, there are some new hotels opening, at last. The Hotel Talatona in Luanda Sul is really nice. Pricey – US$600 for a single room (yes, that’s for one night!) – but the staff know how to smile, and everything appears to work!

Happy Travels- even in Angola!

Trevor

How to make a success of hotel investment?

In Djibouti, the 177 room Kempinski Hotel was built in just nine months. In Accra, the 100 room Labadi Beach Hotel took a little longer, all of 10 months, but still a record-breaking length of time, that would be the envy of any developer in the west.

So why is it that so many hotel projects in sub-Saharan Africa take such a long time to become reality, with several years’ delay by no means unusual? Examples include the Holiday Inn in Accra, in its sixth year of construction, the Radisson SAS in Lagos, due to open in November 2004 and still on-site, and the Hilton in Kampala, due to open in 2007 and still some way from completion.

And what could, what should be done by investors to stop such a waste of opportunity happening on their projects?

In my experience, so much can be laid at the door of a lack of planning. I believe it was Conrad Hilton who said that the three main success factors for a hotel are location, location, location. Well, that’s a good soundbite, oft repeated in the industry, and it does have much to say about the operational success of a hotel. But I think it is planning, planning, planning that marks the success or failure of your development project.

Here are the four main areas where, in my experience, proper planning brings success:

Hotels are difficult, hotels are complex, hotels are big projects. Like in any endeavour, from preparing a meal to landing on the moon, a multitude of skills is required, and the secret of success of projects like the Kempinski in Djibouti is to leverage off the skills of the individual team members. Every developer knows they need an architect – but hotels are not big houses, they are far more complicated, and the architect must have previous experience of proper hotel design.

The project needs managing, and the project manager needs to be involved from the very early design stages. Project management is a skill which requires experience, and rarely, in my experience, does the investor or the architect have that skill, leading to some of the serious delays that we see. Do the maths – a year’s delay in opening a 200 room project, because the project is not properly managed, could mean a loss of in excess of US$10 million in revenue [YOU MIGHT WANT TO PUT A BOX IN TO SUPPORT THIS – SEE THE END OF THIS DOCUMENT].

The international hotel chains have years of experience in hotel design, knowing what works and what does not. The basic objectives of a hotel design are: to deliver what the guest wants; to maximise the revenue-generating possibilities of the building; to minimise the non-revenue generating areas, whilst still providing sufficient support space; to minimise operating expenses; and thereby to maximise the return on the owner’s investment.

When an architect puts the bathrooms on the outside wall, instead of the corridor wall, “for ventilation”, or a toilet in the middle of the kitchen “for when the chef gets caught short”, or omits any staff facilities, you can be sure that the experts have rejected such design elements long ago for good reason. Architects who insist on ignoring conventional wisdom are ensuring that your hotel will be obsolete when it opens, hugely vulnerable to competition.

I know of several hotels, including the Radisson SAS in Lagos and Le Meridien in Port Harcourt, where expert design experience was sought only after starting construction, which brought substantial delays in completion, and cost overruns, which could have been avoided.

So the management company, if one is to be engaged, must be on the team from the get-go – there is absolutely no logical reason why their appointment should be delayed.

As difficult as it may be (and it is arguably getting easier, with new sources of debt and equity available) to fund hotel projects, it is even more difficult to raise money for a half-completed hotel. There are dozens of hotels around Africa, possibly hundreds, where the cost of construction has been underestimated, and funds have run out, or where construction has started without all of the funding in place.

Disruption of the construction due to lack of funds leads to demobilisation of the contractor, the loss of skilled workers, additional cost, completion delays, and lost opportunities. All of which could have been “planned-out” of the process by ensuring from the outset that sufficient funds are available.

And finally, I can come back to the issue of location (times 3!). Many investors seem to believe that, because they own a site, it is suitable for hotel development. Well, not necessarily! Selecting the correct site is part of the planning process – just because demand is high today, and land is hard to come by (a feature of many, many markets in Africa), these are not good reasons to go ahead with a hotel development on a secondary site. Markets are never static, changing over time, and a location which will “do” today, because of high demand and lack of customer choice, is likely to be

at a disadvantage in the future when supply: demand imbalances are evened out. Conversely, locations can change – look at the decline (and subsequent slow reawakening) of the centre of Johannesburg, where the city’s main 5 star hotels were once located – but this tends to be in mature markets.

Many of Africa’s hotel markets are experiencing a shortage of supply in the face of high and increasing demand – e.g. Lagos, Accra, Cape Town, Luanda – and as a result entrepreneurs are rushing in to exploit the situation. Those that plan properly from the outset – getting the design right, putting the funding in place and having the right development team on the project – are creating sustainable businesses. Those that fail to plan, plan to fail.

A hotel with 200 rooms, achieving 50% occupancy in its first year of operation, will sell 36,500 roomnights. At an average daily rate of US$200, that’s rooms revenue of US$7.3 million. With other revenues from meals, drinks and other services, that’s at least US$10 million in total revenue.

Trevor Ward

W Hospitality Group, Lagos

Kenya’s government has been brought to a standstill and finance minister Amos Kimunya has been forced to resign at news that Nairobi’s showpiece Grand Regency hotel was secretly sold to the Libyan Arab Africa Investment Company at a vastly undervalued price. The hotel was sold without negotiation for an official figure of KSh 2.9 billion – a fraction of the KSh 6 billion top-price estimate being bandied about in the media, but the price has caused a storm of debate as to whether the sale price was fair and reasonable or a huge undervaluing of the property.

The scandal highlights how key an issue valuation is in hotel investment and ownership – how does one ensure an accurate price for the investment when one wants to buy, and what constitutes a fair valuation? What influences hotel valuation? There are many factors to take into account when valuing hotels from their capitalization rate and their room rates, as well as on both their historical earnings and on their current and future earnings.

Other factors such as the health of the hospitality industry and political and economic prospects impact values. The bidding process is also crucial – the Grand Regency transaction was particularly hit by accusations of a lack of transparent bidding that could have pushed up the value of the hotel.

This article should outline, using case studies to back up each point, as far as possible, what hotel investors should be aware of when buying into or preparing to sell a hotel property. You could start by discussing Africa’s hotel valuation / sale history? Explain some successful sales or nightmare scenarios for the investors that have hit headlines – like the Regency. What has actually happened there – can you give some insight?

What makes a successful valuation, and how advanced is the industry in Africa? What are the key factors to be noted in this equation? What affects valuations? Who should investors go to for this?

You might want to add in something about who hotel buyers and sellers tend to be in Africa – are they governments, local investors, international groups? Where are these trends headed – towards more local investment, or something else? What’s directing the market?

You might also want to talk about the process of pricing and negotiating a sale – like, what makes an ideal buyer or seller, and what does a viable and mutually profitable deal need to have as its elements?

Offer your experience – where have you seen successes happen and why? What tips would you offer for investors looking for valuation?

This gives a public view on the Regency scandal – you maybe know more about it than this? Do you agree with the writer?

Trevor Ward

W Hospitality Group, Lagos

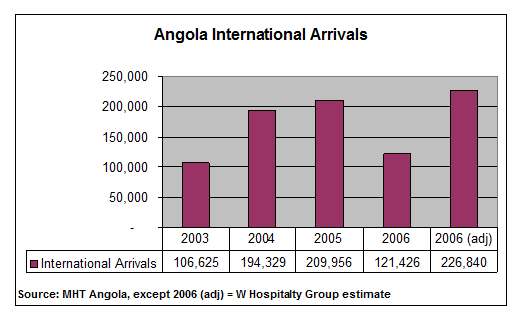

Oil and diamonds drive Angola’s economy, and both commodities are experiencing high prices, resulting in GDP growth at exceptional levels – some 20 per cent in 2007. And this translates directly into demand for hotels. Luanda is experiencing occupancies above 90 per cent year round, with bookings required weeks in advance – and even paying in advance won’t necessarily guarantee you a room!

Tourism figures from the Angola authorities are difficult to reconcile with this surge in demand, reporting a decrease in 2006 – but I believe this is due to a change in counting methodology, excluding those coming in for short-term employment from the figures. More likely there is an increase of at least 10 per cent in arrivals year on year, which is the Ministry of Hotels and Tourism’s forecast for the next 5 years, an estimate more than supported by the very high occupancies experienced by hotels in Luanda and elsewhere, and the high load factors of the incoming airlines.

International investment in Angola is growing, mainly for the reconstruction of the country’s infrastructure and in industry. The main investors are the European Union (EU) and the EU countries individually (mainly Portugal), as well as the USA, China and South Africa.

Over 80 per cent of all arrivals to Angola originate from overseas, while 16 per cent originate from within Africa:

| Angola

Region of Origin, 2005 |

||

| Arrivals | ||

| Europe | 110,025 | 52.4% |

| Africa | 45,100 | 21.5% |

| Americas | 36,140 | 17.2% |

| Asia | 16,748 | 8.0% |

| Middle East | 1,243 | 0.6% |

| Australia | 700 | 0.3% |

| Total | 209,956 | 100.0% |

| Source: MHT | ||

Almost 70 per cent of all arrivals originate from seven countries (2005 data not available):

| Angola

Country of Origin, 2006 |

|

| Portugal | 21% |

| Brazil | 9% |

| UK | 9% |

| South Africa | 8% |

| China | 8% |

| France | 8% |

| USA | 6% |

| Total | 69% |

| Source: MHT | |

The majority of visitors to Angola are entering for business and employment, the latter largely in the oil and gas industry:

| Angola

Reason for Entry, 2005 |

|

| Employment | 69% |

| Leisure and VFR* | 15% |

| Business | 13% |

| Transit | 3% |

| Total | 100% |

| Source: MHT

* – Visiting friends and relatives |

|

Angola has considerable leisure tourism potential, but this is unlikely to be exploited for some years, due to the image of the country, the lack of available air capacity and therefore the high airfares, the cost of hotel and hospitality services, the lack of road infrastructure outside of the main cities, and the proliferation of landmines. Many of the leisure visitors are VFR, from the Diaspora in Portugal and Brazil.

The attractions of Angola, which in the future can be exploited for tourism, include:

| · Beaches

· Sport fishing · Game parks · Adventure tourism |

· History and culture

· Natural landscapes · Bird watching · Whale watching. |

The hotels in Luanda accommodate only very small volumes of leisure travellers, and it is not expected that this market sector will grow in the short- to medium-term.

In response to the high demand, several new projects are underway in Luanda – Korea’s Namkwang are building a 250-room InterContinental Hotel, Sivol a 300-room Hotel Sana (a Portuguese operator and investor), and MITC are the developers of a 64-room extended stay property, a product well suited to the type of demand there.

Outside of Luanda, expect more hotel development in Lobito, where a US$3 billion oil refinery is to be built, and in Soyo, where a US$5 billion LNG plant is under construction. In Soyo, a 100-room hotel is to be built by local investor Dania Comercial, and is reportedly already almost fully taken up with demand from the LNG plant. Benguela has tourism potential, with existing beach resorts attracting demand from Luanda at weekends. Cabinda, the enclave within the territory of the Democratic Republic of Congo, is the centre of Angola’s oil industry, and there are plans for massive investment in housing and hotels there.

Such tourism as has been developed is mostly in the south of the country (Namibe Province), with demand generated by the South African and Namibian markets, who drive into the country and visit the game parks and participate in adventure activities in the desert. Road and air access from Luanda has improved recently. The two existing hotels have insufficient capacity for expected growth in demand.

The Angolan authorities are keen to expand the tourism industry, in order to diversify the economy away from primary products, and to take advantage of the country’s natural assets which, due to previous internal problems, have been virtually unexploited. Investment in tourism will bring considerable benefits to the population in rural areas, who see little benefit from the oil industry.

The following data on the number of international arrivals in Angola have been provided by the Ministry of Hotels and Tourism (MHT):

Whilst the reduction in arrivals in 2006 reported by the Ministry is said to be due to a reduction in major conferences compared to 2005, an analysis of the detailed data reveals that the actual reason appears to be a change in methodology of data capture – almost the entire reduction is due to a reduction in the number of migrant workers, a proportion of whom are clearly no longer counted as arrivals. Applying 8 per cent growth to the 2005 figure (2005 was 8 per cent higher than 2004) results in a figure of approximately 227,000 visitors in 2006 (shown above as “2006 adj”), an increase which is conservative and more than supported by the very high occupancies experienced by hotels in Luanda and elsewhere, and the high load factors of the incoming airlines.

Trevor Ward

W Hospitality Group, Lagos

Long-dominated by the luxurious Sheraton Hotel, Addis Ababa is seeing a huge expansion in its hotel stock currently, with at least 1,250 mid-market to upscale new rooms actually under construction, and a further 800 to 1,000 in the planning stages. The Sheraton, and the other branded hotel, the somewhat aged Hilton, are likely to be joined by Holiday Inn, Radisson, Marriott, Ibis, Novotel and Four Points in the very near future.

Driving this boom is a rapid emergence from Ethiopia’s dark years, and particularly greater confidence in the economy on the part of the large and successful Ethiopian Diaspora. Addis Ababa is one of Africa’s primary administrative centres, the home of the African Union and the United Nations’ Economic Commission for Africa. Ethiopia is an attractive country from an investor’s point of view, with its population of 77 million providing an inexpensive, well-educated and trainable labour force. It is strategically located at the crossroads between Africa, the Middle East and Asia.

Agriculture is one of the country’s most promising resources. The potential exists for self-sufficiency in grains and for export development in livestock, vegetables and fruits. Agriculture employs 80 per cent of the work force, and accounts for half of Ethiopia’s GDP and 60 per cent of its exports. Even though most production is at a subsistence level, large parts of commodity exports are provided by the small agricultural cash crop sector. Many other economic activities depend on agriculture, including marketing, processing and exportation.

Ethiopia’s economic growth averaged 8.6 per cent (source: OECD) between 2004 and 2006, driven by agriculture as well as expansion in industry and services. Other sources report economic growth of 10 per cent for the past two years. The World bank is forecasting 9 per cent annual GDP growth to 2010.

Business and conference demand accounts for some 75 per cent of the total demand for hotel accommodation in Addis Ababa and, unlike many African cities which rely almost entirely on the commercial market, the city enjoys a high level of demand from the leisure sector, approximately 16 per cent of total demand.

Ethiopia is shaking off its negative images, and having some success in the specialist leisure market, particularly travellers looking for a unique combination of adventure, history, natural wonder and religion. Addis Ababa boasts several historic sites, such as St Georges Cathedral and the Menelik Mausoleum, but it is in the north and the south of the country that the main attractions lie, including the Northern Circuit, taking in such wonders as the sunken churches at Lalibela, and the Rift Valley to the

south, a birding paradise. With the increase in tourists coming through Addis Ababa, local entrepreneurs such as Tadiwos Belete of Boston Partners, and Sheikh Al Amoudi of Midroc are investing in eco lodges around the country, tapping into their own resources as well as the Diaspora.

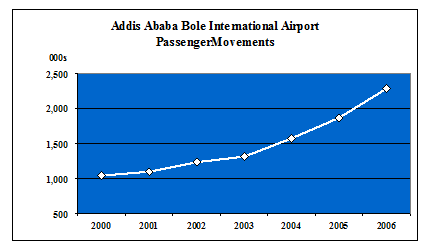

In addition to demand from business and other visitors to the country itself, Addis Ababa’s new airport is attracting increasing numbers of transit passengers, with Ethiopian Airlines having one of the best hubs in Africa. Troubles in neighbouring Kenya, and increasing crime at Johannesburg airport, have heightened the appeal of Addis Ababa as a transit hub. This activity generates considerable demand for hotel accommodation, and Ethiopian Airlines, in partnership with Chinese investors, is planning a new hotel at the airport to accommodate that demand.

Passenger traffic at the airport grew at an average of around 20 per cent in the last three years (2004 to 2006, latest data available), and by 120 per cent since 2000; growth is forecast to be 13 per cent into the near future – Ethiopian Airlines will be the first in Africa to fly the new state-of-the-art Boeing Dreamliner.

For the country as a whole, international arrivals increased by 29 per cent in 2006 to almost 300,000, again more than double the 2000 figure. Preliminary estimates for 2007 are for a significant further increase, due to the celebrations for Ethiopia’s Millennium.

Occupancies in Addis Ababa averaged around 80 per cent in 2007 and, with demand growth forecasts of 8 to 10 per cent annually, much of the future supply should be able to be absorbed without a problem. As is so often found in markets such as this, the internationally-branded hotels will achieve higher occupancies and rates than the locally managed ones, with the exception of the small boutique hotels that find their special market niche. The State-owned Ghion chain of hotels has been the subject of privatisation rumours for many years, and it is hoped that the government’s reluctance to do a deal to date will be overcome as more competition enters the market.

TOURISM AND HOTEL STATISTICS

| International Traffic Movements at Bole

(Arrivals and Departures) |

|||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | |

| Passengers | 1,037,976 | 1,096,605 | 1,237,858 | 1,314,740 | 1,573,330 | 1,869,930 | 2,287,544 |

| Growth (%) | – | 5.6 | 12.8 | 6.2 | 19.6 | 18.8 | 22.3 |

| Source: Ethiopian Airports Enterprise | |||||||

| Addis Ababa

Ethiopian Airlines Scheduled Passenger Movements |

|||||

| Year | Domestic | International | Ethiopian Total | Bole International Total* | Ethiopian Share (%) |

| 2003/04 | 231,797 | 918,067 | 1,149,864 | 1,314,740 | 87.5 |

| 2004/05 | 253,037 | 1,186,754 | 1,439,791 | 1,573,330 | 91.5 |

| 2005/06 | 257,844 | 1,392,409 | 1,650,253 | 1,869,930 | 72.2 |

| 2006/07 | 257,282 | 1,730,932 | 1,988,214 | 2,287,544 | 86.9 |

| Source: Ethiopian Airlines HQ/Ethiopian Airports Enterprise

* Calendar years 2004 to 2006 |

|||||

| Addis Ababa

Transit Passenger Trends 2002 2006 |

|||

| 2004 | 2005 | 2006 | |

| January | 6,235 | 9,122 | 9,514 |

| February | 4,024 | 6,093 | 5,399 |

| March | 4,188 | 4,201 | 6,272 |

| April | 5,762 | 6,119 | 6,920 |

| May | 6,432 | 5,934 | 6,956 |

| June | 6,184 | 8,022 | 7,780 |

| July | 7,608 | 11,505 | 9,857 |

| August | 7,672 | 11,053 | 10,278 |

| September | 7,145 | 6,678 | 9,951 |

| October | 5,545 | 6,959 | 8,281 |

| November | 5,691 | 7,092 | 7,721 |

| December | 6,052 | 11,252 | 10,591 |

| Total | 72,538 | 94,030 | 99,520 |

| Daily Average | 198.7 | 257.6 | 272.6 |

|

Source: Ethiopian Airlines |

|||

Long-dominated by the luxurious Sheraton Hotel, Addis Ababa is seeing a huge expansion in its hotel stock currently, with at least 1,250 mid-market to upscale new rooms actually under construction, and a further 800 to 1,000 in the planning stages. The Sheraton, and the other branded hotel, the somewhat aged Hilton, are likely to be joined by Holiday Inn, Radisson, Marriott, Ibis, Novotel and Four Points in the very near future.

Driving this boom is a rapid emergence from Ethiopia’s dark years, and particularly greater confidence in the economy on the part of the large and successful Ethiopian Diaspora. Addis Ababa is one of Africa’s primary administrative centres, the home of the African Union and the United Nations’ Economic Commission for Africa. Ethiopia is an attractive country from an investor’s point of view, with its population of 77 million providing an inexpensive, well-educated and trainable labour force. It is strategically located at the crossroads between Africa, the Middle East and Asia.

Agriculture is one of the country’s most promising resources. The potential exists for self-sufficiency in grains and for export development in livestock, vegetables and fruits. Agriculture employs 80 per cent of the work force, and accounts for half of Ethiopia’s GDP and 60 per cent of its exports. Even though most production is at a subsistence level, large parts of commodity exports are provided by the small agricultural cash crop sector. Many other economic activities depend on agriculture, including marketing, processing and exportation.

Ethiopia’s economic growth averaged 8.6 per cent (source: OECD) between 2004 and 2006, driven by agriculture as well as expansion in industry and services. Other sources report economic growth of 10 per cent for the past two years. The World bank is forecasting 9 per cent annual GDP growth to 2010.

Business and conference demand accounts for some 75 per cent of the total demand for hotel accommodation in Addis Ababa and, unlike many African cities which rely almost entirely on the commercial market, the city enjoys a high level of demand from the leisure sector, approximately 16 per cent of total demand.

Ethiopia is shaking off its negative images, and having some success in the specialist leisure market, particularly travellers looking for a unique combination of adventure, history, natural wonder and religion. Addis Ababa boasts several historic sites, such as St Georges Cathedral and the Menelik Mausoleum, but it is in the north and the south of the country that the main attractions lie, including the Northern Circuit, taking in such wonders as the sunken churches at Lalibela, and the Rift Valley to the

south, a birding paradise. With the increase in tourists coming through Addis Ababa, local entrepreneurs such as Tadiwos Belete of Boston Partners, and Sheikh Al Amoudi of Midroc are investing in eco lodges around the country, tapping into their own resources as well as the Diaspora.

In addition to demand from business and other visitors to the country itself, Addis Ababa’s new airport is attracting increasing numbers of transit passengers, with Ethiopian Airlines having one of the best hubs in Africa. Troubles in neighbouring Kenya, and increasing crime at Johannesburg airport, have heightened the appeal of Addis Ababa as a transit hub. This activity generates considerable demand for hotel accommodation, and Ethiopian Airlines, in partnership with Chinese investors, is planning a new hotel at the airport to accommodate that demand.

Passenger traffic at the airport grew at an average of around 20 per cent in the last three years (2004 to 2006, latest data available), and by 120 per cent since 2000; growth is forecast to be 13 per cent into the near future – Ethiopian Airlines will be the first in Africa to fly the new state-of-the-art Boeing Dreamliner.

For the country as a whole, international arrivals increased by 29 per cent in 2006 to almost 300,000, again more than double the 2000 figure. Preliminary estimates for 2007 are for a significant further increase, due to the celebrations for Ethiopia’s Millennium.

Occupancies in Addis Ababa averaged around 80 per cent in 2007 and, with demand growth forecasts of 8 to 10 per cent annually, much of the future supply should be able to be absorbed without a problem. As is so often found in markets such as this, the internationally-branded hotels will achieve higher occupancies and rates than the locally managed ones, with the exception of the small boutique hotels that find their special market niche. The State-owned Ghion chain of hotels has been the subject of privatisation rumours for many years, and it is hoped that the government’s reluctance to do a deal to date will be overcome as more competition enters the market.

TOURISM AND HOTEL STATISTICS

| International Traffic Movements at Bole

(Arrivals and Departures) |

|||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | |

| Passengers | 1,037,976 | 1,096,605 | 1,237,858 | 1,314,740 | 1,573,330 | 1,869,930 | 2,287,544 |

| Growth (%) | – | 5.6 | 12.8 | 6.2 | 19.6 | 18.8 | 22.3 |

| Source: Ethiopian Airports Enterprise | |||||||

| Addis Ababa

Ethiopian Airlines Scheduled Passenger Movements |

|||||

| Year | Domestic | International | Ethiopian Total | Bole International Total* | Ethiopian Share (%) |

| 2003/04 | 231,797 | 918,067 | 1,149,864 | 1,314,740 | 87.5 |

| 2004/05 | 253,037 | 1,186,754 | 1,439,791 | 1,573,330 | 91.5 |

| 2005/06 | 257,844 | 1,392,409 | 1,650,253 | 1,869,930 | 72.2 |

| 2006/07 | 257,282 | 1,730,932 | 1,988,214 | 2,287,544 | 86.9 |

| Source: Ethiopian Airlines HQ/Ethiopian Airports Enterprise

* Calendar years 2004 to 2006 |

|||||

| Addis Ababa

Transit Passenger Trends 2002 2006 |

|||

| 2004 | 2005 | 2006 | |

| January | 6,235 | 9,122 | 9,514 |

| February | 4,024 | 6,093 | 5,399 |

| March | 4,188 | 4,201 | 6,272 |

| April | 5,762 | 6,119 | 6,920 |

| May | 6,432 | 5,934 | 6,956 |

| June | 6,184 | 8,022 | 7,780 |

| July | 7,608 | 11,505 | 9,857 |

| August | 7,672 | 11,053 | 10,278 |

| September | 7,145 | 6,678 | 9,951 |

| October | 5,545 | 6,959 | 8,281 |

| November | 5,691 | 7,092 | 7,721 |

| December | 6,052 | 11,252 | 10,591 |

| Total | 72,538 | 94,030 | 99,520 |

| Daily Average | 198.7 | 257.6 | 272.6 |

| Source: Ethiopian Airlines | |||

| Ethiopia

International Tourist Arrivals and Receipts |

||||

| Arrivals | Growth (%) | Receipts (US$m) | Growth (%) | |

| 2000 | 135,954 | – | 62.8 | – |

| 2001 | 148.438 | 9.2 | 69.8 | 11.1 |

| 2002 | 156,327 | 5.3 | 73.5 | 5.3 |

| 2003 | 179,910 | 15.1 | 84.6 | 15.1 |

| 2004 | 184,078 | 2.3 | 107.7 | 27.3 |

| 2005 | 227,389 | 23.5 | 128.0 | 28.1 |

| 2006 | 290,458 | 27.7 | 138.9 | 8.5 |

| Sources: Ministry of Culture and Tourism

Addis Ababa Tourism Commission |

||||

It should be noted, however, that tourism statistics in many countries, including Ethiopia, are open to question, due to the methodologies of collection. It is likely that the data for 2002 and 2003 have been estimated, as evidenced by the same growth figures for arrivals and receipts in 2002 and 2003. However, the general trend in arrivals is extremely positive, and matches the data gathered at the airport. The data show significant increases from 2004 which coincides with the opening of the new Bole Airport Terminal. The Ethiopian Diaspora has also increased its traffic back to the country, as the country improves and is more conducive for inward investment.

| Ethiopia

Monthly arrivals 2005-2006, Bole International Airport |

|||

| Month | 2005 | 2006 | % change |

| January | 15,029 | 26,360 | 75.3 |

| February | 13,419 | 21,185 | 57.8 |

| March | 15,070 | 21,984 | 45.8 |

| April | 18,992 | 24,062 | 26.6 |

| May | 14,602 | 25,105 | 71.9 |

| June | 20,619 | 26,102 | 26.5 |

| July | 21,354 | 27,770 | 30 |

| August | 22,039 | 25,765 | 16.9 |

| September | 25,537 | 25,005 | -2.08 |

| October | 25,484 | 24,700 | -3.07 |

| November | 16,513 | 22,515 | 36.3 |

| December | 18,740 | 19,995 | 6.6 |

| Total | 227,398 | 290,458 | 27.7 |

| Source: Min Culture and Tourism | |||

The diagram below shows data for purpose of visit in 2006, based on statistics provided by the Addis Ababa Tourism Commission:

Region of origin data of visitors to Ethiopia for 2006 are as follows:

| Ethiopia

Region of Origin, 2006 |

||

| Continent | Arrivals | % |

| Africa | 89,923 | 30.9 |

| Europe | 76,466 | 26.3 |

| North America | 61,353 | 21.1 |

| Middle East | 30,556 | 10.5 |

| Asia | 28,033 | 9.6 |

| Oceania | 4,127 | 1.4 |

| Total | 290,248 | 100 |

| Source: Addis Ababa Tourism Commission | ||

| Ethiopia

Inbound Tourists by Country of Residence |

|||||

| Country | 2003 | 2004 | 2005 | 2006 | Change

2003-2006 |

| USA | 26,399 | 28,112 | 32,282 | 43,610 | 65.2% |

| UK | 8,919 | 10,627 | 11,254 | 16,076 | 80.2% |

| China | 3,318 | 4,172 | 7,649 | 10,445 | 214.8% |

| Kenya | 7,481 | 7,217 | 9,277 | 8,690 | 16.2% |

| Saudi Arabia | 10,503 | 9,778 | 5,382 | 8,463 | -19.4% |

| Italy | 6,505 | 7,696 | 7,983 | 8,386 | 28.9% |

| India | 4,276 | 4,616 | 7,125 | 7,975 | 86.5% |

| Germany | 5,611 | 6,256 | 6,731 | 7,428 | 32.4% |

| Canada | 5,013 | 5,169 | 8,396 | 7,349 | 46.6% |

| France | 4,380 | 4,501 | 5,800 | 6,649 | 51.8% |

| Nigeria | 3,850 | 3,415 | 5,524 | 6,513 | 69.2% |

| Sweden | 3,153 | 3,336 | 4,342 | 6,337 | 101.0% |

| Israel | 2,965 | 3,874 | 5,291 | 5,556 | 87.4% |

| Source: Min Culture and Tourism | |||||

A 2006 World Bank study of how to grow the tourism industry in Ethiopia highlighted a current lack of private investment and government dominance in the accommodation sector resulting in a lack of high quality accommodation and services. that study provided the following data.

| Addis Ababa

Tourist Expenditure and Foreign Exchange Receipts |

||||||

| Purpose of Visit | Numbers of Visitors | Average Length of Stay | Average Spend per Day US$ | Average Spend Per Visit US$ | Total Spend per Sector US$ | |

| Business | 46,008 | 4.4 days | 113.89 | 501.12 | 23,055,529 | |

| Vacation | 63,246 | 8.6 days | 123.56 | 1,062.66 | 67,208,994 | |

| Conference | 16,385 | 2.8 days | 109.80 | 307.44 | 5,037,404 | |

| VFR* | 21,738 | 17.9 days | 33.89 | 606.63 | 13,186,923 | |

| Subtotal | 147,377 | 108,488,850 | ||||

| Not Stated | 30,469 | 803.29 | 24,475443 | |||

| Totals | 177,846 | 656.22 | 132,944,293 | |||

| Source: World Bank

*Visiting Friends and Relatives. |

||||||

These data should be regarded as indicative only – they are collected from the forms completed on hotel check-in. Some guests do not complete the forms at all, and we understand where the field for purpose of visit is not completed, the compilers of the statistics record it as ‘other’.

| Addis Ababa

Existing Hotel Supply – Published Rates (including breakfast, excluding 10% Service Charge and 15% VAT) |

|||||||

| Hotels of Primary Relevance | Tariffs US$ | ||||||

| Rooms | Single | Double | Executive Single | Executive Double | Suite Single | Suite Double | |

| Sheraton Addis | 295 | 375 | 420 | 425 | 470 | 795 | 795 |

| Hilton Addis Ababa* | 350 | 195 | 210 | 220 | 235 | 265 | 265 |

| Ghion Hotel | 190 | 69 | 85 | 110 | – | – | – |

| Hotels of Secondary Relevance | Tariffs US$ | ||||||

| Rooms | Single | Double | Executive Single | Executive Double | Suite Single | Suite Double | |

| Hotel De Leopol | 74 | 48 | 68 | 162- | 213- | – | – |

| Atlas Hotel | 67 | 70 | 80 | 80 | – | 150 | – |

| Axum Hotel | 64 | 50-66 | 60-66 | 66-90 | 72-90- | 102 | – |

| Imperial Hotel | 63 | 66 | 84 | – | – | 114 | – |

| Ambassador Suites | 52 | – | – | – | – | 86-111 | – |

| Global Hotel | 55 | 75 | – | 101 | – | 127- | – |

| Queen of Sheba | 45 | 71 | – | 88 | – | – | – |

| Source: W Hospitality Group Research

*the Hilton includes breakfast only in its executive room and suite rates |

|||||||

| Addis Ababa

Roomnight Demand and Market Mix (2007) |

||

| Market Sector | Roomnights | Market Mix |

| Business | 173,453 | 49.7% |

| Conference | 93,098 | 26.7% |

| Aircrew | 4,576 | 1.3% |

| Airport related | 22,269 | 6.4% |

| Leisure | 55,314 | 15.9% |

| Total Demand | 348,710 | 100.0% |

| Addis Ababa

Future Hotel Projects |

|||

| Projects | Rooms | Status | Estimated Opening Date |

| Jupiter Hotel | 40 | Near completion | Q2 – 2008 |

| Zenebat | 80 | Under construction | 2009 |

| Debrea Damo | 80 | Under construction | mid-2009 |

| Intercontinental (SIMEX) | 151 | Work stopped | 2010 |

| Sunshine | 250 | Studies in progress | 2010 |

| Emerald | 168 | Work stopped | 2010 |

| Sheraton (Extension) | 200 | Studies in progress | 2010 |

| Jupiter Hotel 2 | 102 | Under construction | 2010 |

| Ibis | 140 | Under construction | mid-2010 |

| Novotel | 100 | Under construction | mid-2010 |

| African Union | 200 | Work commenced | mid-2010 |

| CATIC | 325 | Studies in progress | 2011 |

| Kenenisa Bekele | 75 | Site identified | 2011 |

| Four Points | 200 | Site identified | 2012 |

| Total | 2,111 | ||

| Source: W Hospitality Group Research | |||

There are just over 2,100 new hotel rooms planned or under construction in Addis Ababa,. However, some of these projects have been on the drawing board for years and most were supposed to have been completed in anticipation of the Ethiopian Millennium celebrations in 2007 – which has come and gone.

It is evident from observation on the ground in Addis Ababa that commencement of construction does not necessarily mean that the hotel will be completed on time, if at all. Only time will tell whether all of the above hotels will materialise. It is logical to assume that hotels such as the Ibis and the Novotel will proceed to realisation within the planned timeframe, as the promoters have financial substance. Whether the same can be said of the other hotels under construction, such as the Simex and Emerald, is unclear. What is clear is that the promoters were, for whatever reason, unable to meet their planned realisation date, and that must cast doubt regarding the future of the projects.

Trevor Ward

W Hospitality Group, Lagos